After a five-year period of sustained growth, it seems there is now a change in the air. Whether they are early tidings of a general cyclical shift, a result of factors such as Brexit or something more local in nature, there are some signs that are urging us to take our foot off the accelerator and take stock, to better to judge the prevailing conditions.

Looking ahead – what’s in store for the market?

The figures tell us that 2018 was another year in a series that started – at least in the Marbella area – around 2013. Here the market bottomed out in 2012 and began a gradual recovery in 2013 that had accelerated into a new growth cycle by 2015, with strong demand for the new modern villas and apartments being built both then and now.

This shift of focus from looking for cheaper distressed buys to wanting off-plan lifestyle properties with all the latest mod cons happened later in other parts of the Costa del Sol and across the country, where Madrid, Barcelona and then Valencia followed the early recovery of Marbella, Mallorca and Ibiza. Here too, price drops had not been as extreme as in other parts of Spain.

In a country of this size and diverse market segments, some regions are only now beginning to feel the effects of recovery, just as others fear their property sector might be peaking. Across Spain, sales rose 11,3% in 2018 compared with 2017, while in Andalucía the increase was 13,8% and in the province of Málaga 7,4%.

The above seems to confirm that while some regions, including Andalucía, are still in full upswing, others are beginning to see a slowing down of growth. With a widely reported drop-off in enquiries and sales in H2 of last year, albeit with a rallying of activity towards the end of the year, this appears to apply to Marbella and the Costa del Sol, which drive much of the growth in Málaga province – itself consistently one of the most important and dynamic property markets in Spain.

“…while some regions, including Andalucía, are still in full upswing, others are beginning to see a slowing down of growth.”

Where the market is at

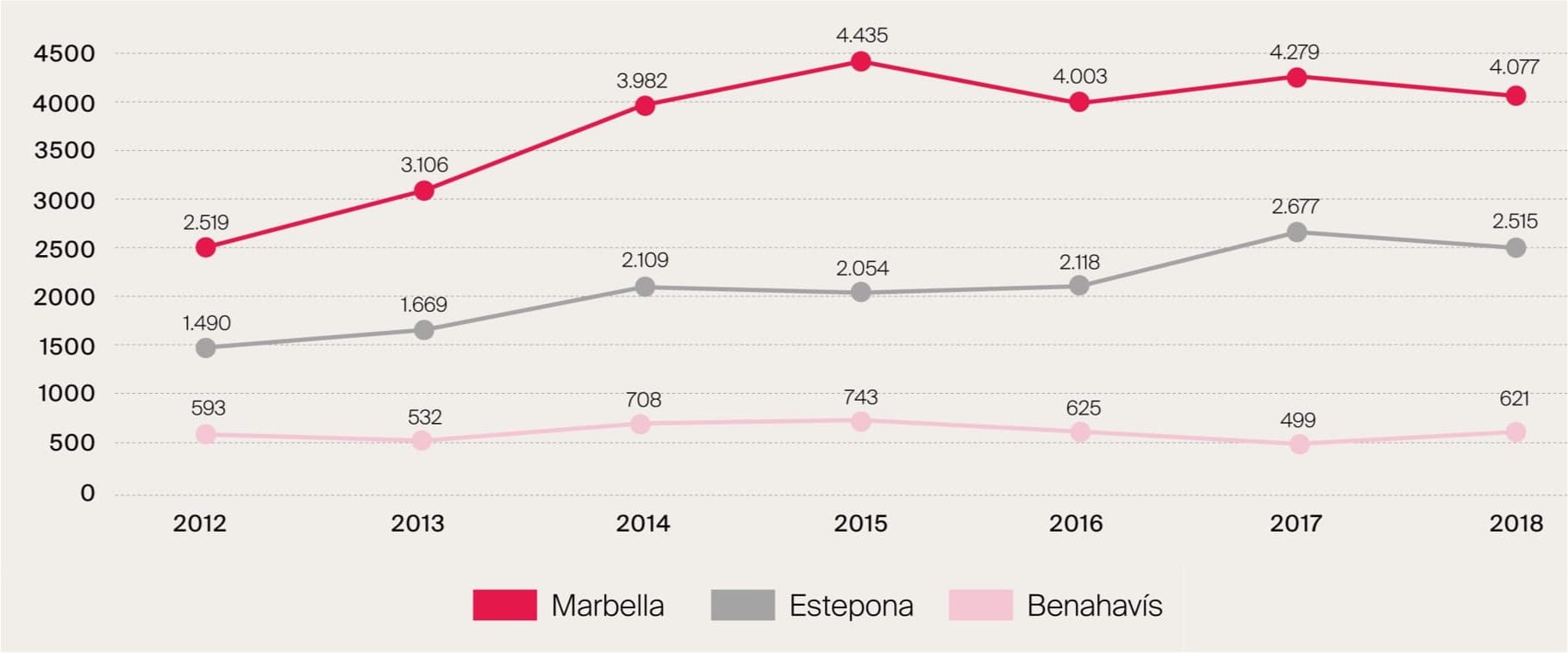

Sales for the so-called Golden Triangle (Marbella, Estepona and Benahavís) had been rising since 2011, with the exception of a small dip in 2016 caused by the after-shock of the Brexit referendum in H2 of the year. The number of transactions registered rebounded in 2017, with strong international demand and a resurgent British market, yet in 2018 it stabilised due to a relatively poor showing in the second half of the year.

Growth levelling off

Agents in the region reported a pick-up in enquiries at the end of the year, but by and large the stabilisation has continued into 2019. What does this mean? Not necessarily anything too ominous, as it wouldn’t be such a bad thing if we were to hold on to the present level of sales activity, but in reality, a slow-down in growth is usually followed by a drop, not an extended period of level activity. It’s therefore important to look at the possible causes behind the latest trend.

Las Brisas, Frontline golf course villa – DM4484

Marbella’s tourist and property segments were among the early lights leading the Spanish economy back to growth levels that have been hovering between 2,5-3% for some years now. The unemployment rate, indebtedness and also public debt have gradually declined, and the overall outlook for the country is reasonably good, albeit with the same downward growth forecast that affects many countries around the world right now.

Marbella is a bit of a national indicator, as it tends to be ahead of the curve economically, and it’s in part due to the fact that it is so dependent upon and in tune with the broader European economies. Demand from these sources has been solid for some time now, driven primarily by new-build modern homes and – in spite of the fact that banks are lending again and interest rates are at historic lows – predominantly by cash buyers. And yet, just lately there has been a tailing off of demand, which seems to indicate something is afoot.

Property sales in ‘The Golden Triangle’ show a 56% increase from 2012 to 2018*

*Provisional, unconfirmed figures for the fourth quarter 2018

Source: Ministerio de Fomento

The factors at play

It is tempting to look straight to Brexit and gathering macroeconomic clouds for an answer, but before we do let’s analyse things closer to home. More specifically, let’s look at the interaction between the main factors at work in our market, namely: Supply, Demand, Price, Cost and Planning.

We can all agree that there has been a ‘white revolution’ of modern styled properties on the coast since the construction machine cranked back into life around 2012. The first new projects sold so well that it became clear there was a shortage of such homes relative to an eager demand for the latest styles, build qualities and high-tech amenities, but now we seem to be approaching a situation where supply has caught up with demand and is in danger of surpassing it. This is nothing new, as we’ve experienced it before, and it seems to be confirmed by a record number of new projects in Málaga province being signed off by the Colegio de Arquitectos (Institute of Chartered Architects) in 2017, and then again in 2018, when it increased by 57%.

Over-supply?

With a slight time-lag, this translates into a record number of new projects entering the market, and while they are mostly smaller in scale than during the boom of the 2000s, there is a worrying lack of variety, as many seem to focus on the same mix of design, amenities and price range. Feedback from the market is that the greatest drop in sales has been seen in the lower-to-mid range, which appears to be suffering from a degree of oversupply and over-competition. The more idiosyncratic offering of the top-end of the market looks to be more robust, and those brave enough to veer away from the lowest common denominator are finding rewarding niche segments in the market, though in Marbella, where there is in fact a shortage of new projects, the scenario is quite different.

Price and cost

It therefore appears that, external factors aside, there is a strong appetite for the lifestyle and properties of this region, but that oversupply and high prices are beginning to have an adverse impact on the market. Earlier projects saw developers buy the best plots of land cheap, build at a lower cost and sell faster, yet now land values have risen faster than the properties built on them, construction costs are similarly putting pressure on investors’ margins, and the rising house and square metre prices are beginning to put buyers off – especially in a market with so much choice and the best locations taken.

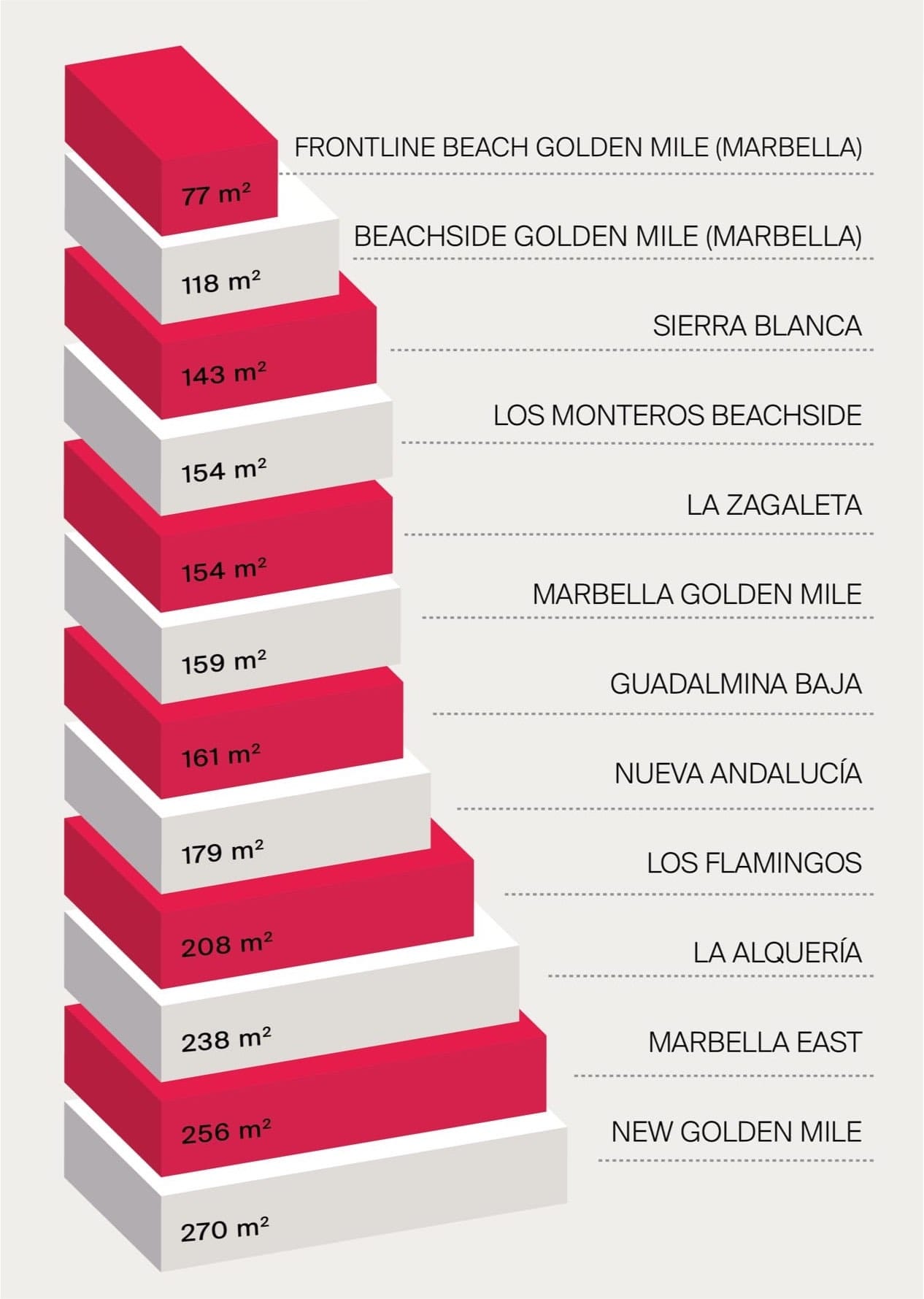

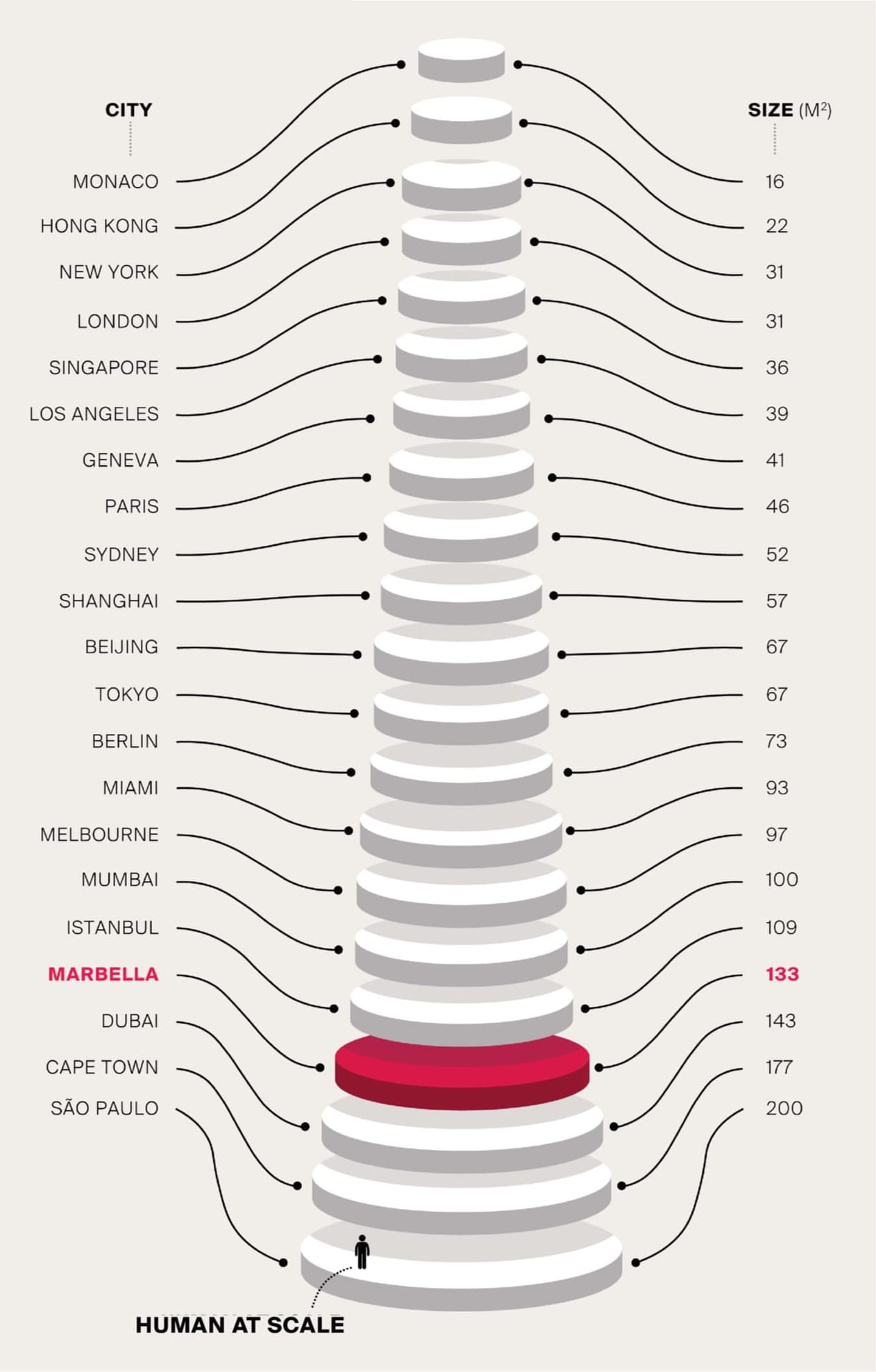

Comparative values in the Golden Triangle (Marbella, Estepona, Benahavís)

How many square metres does 1.000.000€ buy.

Source: DM Properties Knight Frank

Value

High prices are not sexy unless you’re in a rapidly upwardly mobile economy, and while top-end buyers are willing to pay a premium for well-located modern villas and apartments that offer true villa specifications, the recent rise in popularity of cheaper areas such as Manilva indicates that the lower half of the market is coming full-circle and searching for value in the form of repurposed, previously unsold stock of the kind being snapped up in and around Marbella between 2010 and 2014. The surrounding areas have recovered more slowly than Marbella, but they are also drawing buyers through attractive prices in a Costa del Sol market that seems to be losing the battle against value, as the average price increase in 2018 ranged from 3% to 7% depending on location and property type within the Marbella area.

Off-plan versus Re-sale

If it was modern off-plan developments that have been driving the market in recent years, they are also the ones whose prices (especially per m2) have been growing fastest. This is partly driven by consumer demand, partly by rising producer costs and also by the mechanism of raising prices between successive stages of a project. The latter, like flipping, can only be maintained in a buoyant market, and adds to the latest trend away from off-plan domination and back towards re-sales. The latter are seen to offer more m2 for your euro, and often in established areas. For whereas the recent cycle has seen a great increase in activity both with new and resale properties in the New Golden Mile, La Alquería, Los Flamingos, Atalaya, Nueva Alcántara and La Cala de Mijas as new property hotbeds, it will take more than one growth cycle to truly cement their reputation.

La Alqueria, State of the art Modern Family Home – DM4230-01

Modernising existing stock

Quite apart from hitherto unsold repossessions, the market for renovating and modernising older properties is one that remains solid and is in fact gaining in popularity again. This is because people are seeing more potential value in it, and it will remain a solid segment as long as selling prices and renovation costs do not grow so quickly as to render the option increasingly unattractive. The success both private investors/homeowners and specialised businesses have had with updating existing villas and even apartments, shows that the buying public will certainly consider a re-sale property as long as you make it sexy and appealing. In fact, just lately there seems to be a little fatigue with modern white minimalist styles, so people seem to be more open to classic-contemporary blends than they have been for a while, yet modern infrastructure and amenities as well as build qualities remain high on most buyers’ wish lists. Consequently, companies dedicated to the complete refurbishment of second-hand properties have been successful mainly in well-established areas such as Nueva Andalucía and the Marbella Golden Mile.

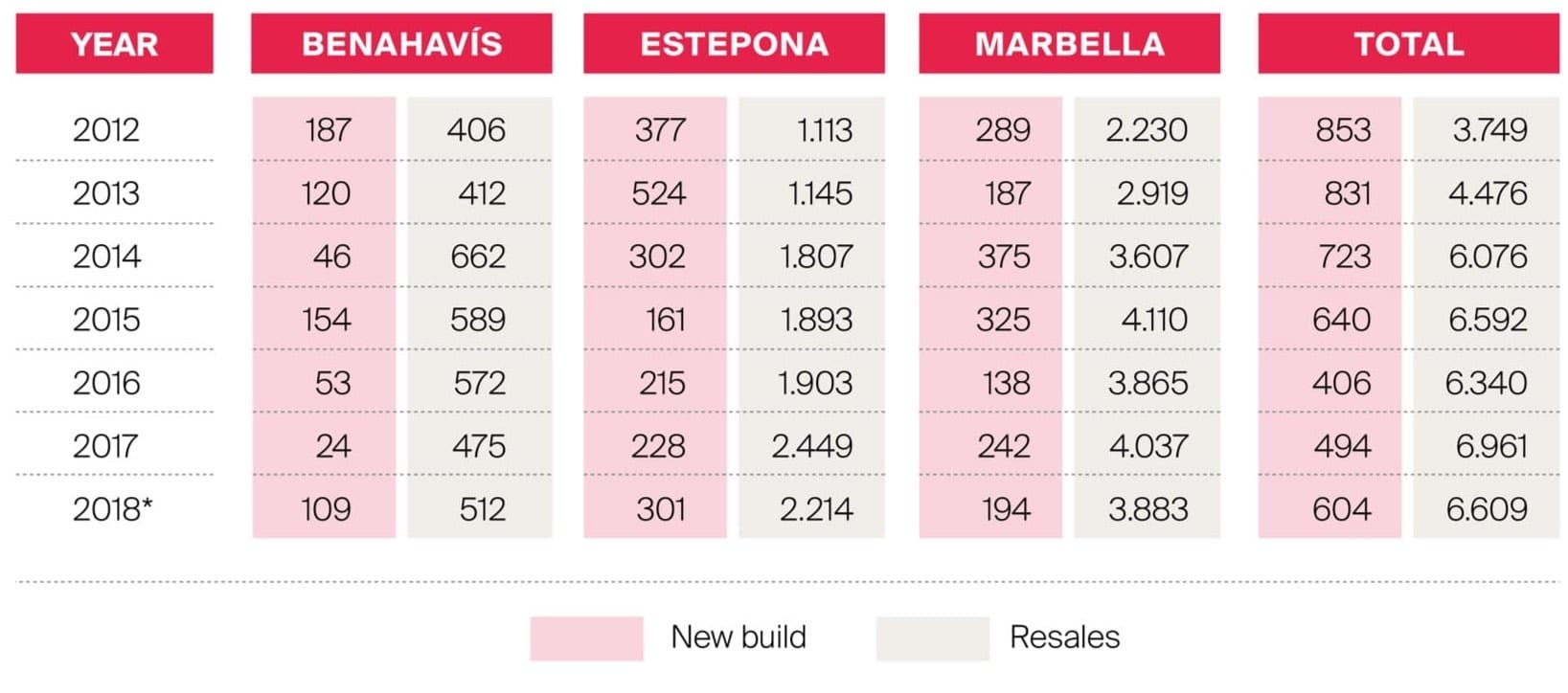

New build vs Resales 2012-2018 by municipality

Provisional, unconfirmed figures for the fourth quarter 2018

Source: Ministerio de Fomento

Product trends

In addition to modern build standards, open-plan living, terrace pools and/or jacuzzis, entertainment areas, home automation systems, fast WiFi and 24-hour security, other features that are gaining ground are concierge services, ever more sophisticated spas and even such elements as lagoon-style communal pools, clubhouses and private residents-only parks and green zones. Environmental credentials and energy-efficient homes are also more important than before, with indigenous Mediterranean landscaping winning out over subtropical gardens and some developments even incorporating organic vegetable plots into an overall philosophy of wellbeing that adds a new element to the traditional glamorous lifestyle appeal of Marbella. Due to the increasing general awareness towards sustainable materials and environmental preservation, we will no doubt see more eco-friendly construction in the years to come.

Value-added locations

Location is the king of real estate, and while we’ve not yet seen the cross-branded luxury residence that is taking foot in luxury markets elsewhere (think Armani villas or Cartier apartments), it is true that a property that carries the signature of a ‘starchitect’ or could boast to be a product of Porsche Design, would carry more allure and a higher price tag. This is also true of sea or waterside views, which can fetch up to 25% more for an intrinsically similar home, while golf and country club locations like branded properties can add 15% to the value. The Kempinski resort in Estepona was the pioneer in the area back in 1999 and it will be joined by the Costa del Sol Princess in Estepona, while Marbella will soon see the opening of Club Med as well as Four Seasons and W Hotel, which will both be offering branded residences as well as hotel rooms.

La Cerquilla, Stylish frontline golf villa – DM2626

New versus established areas

At the end of the day, limited supply combined with a frontline beach location and lots of pedigree makes the Golden Mile a prime address that has recently been capable of square metre prices in excess of €20,000. Other established areas are similarly still much in demand, and while much of the recent growth has been in up-and-coming zones such as the New Golden Mile, Estepona West, Marbella East and La Cala, they still have some catching up to do in terms of intrinsic appeal, since their recent competitive advantage has been more about availability of land and building licences, as well as value for money.

The Golden Triangle

While Marbella solves its planning issues, Benahavís, Estepona, Ojén and Mijas have stepped in to absorb much of the recent growth in what can generally be described as a broadly beneficial spreading of development and investment. It has levelled the playing field a little and given developer and buyer alike a broader range of options than before. For now, however, we’re witnessing a cooling off of demand in the new areas, as they too see prices rise perhaps more quickly than the market can carry right now.

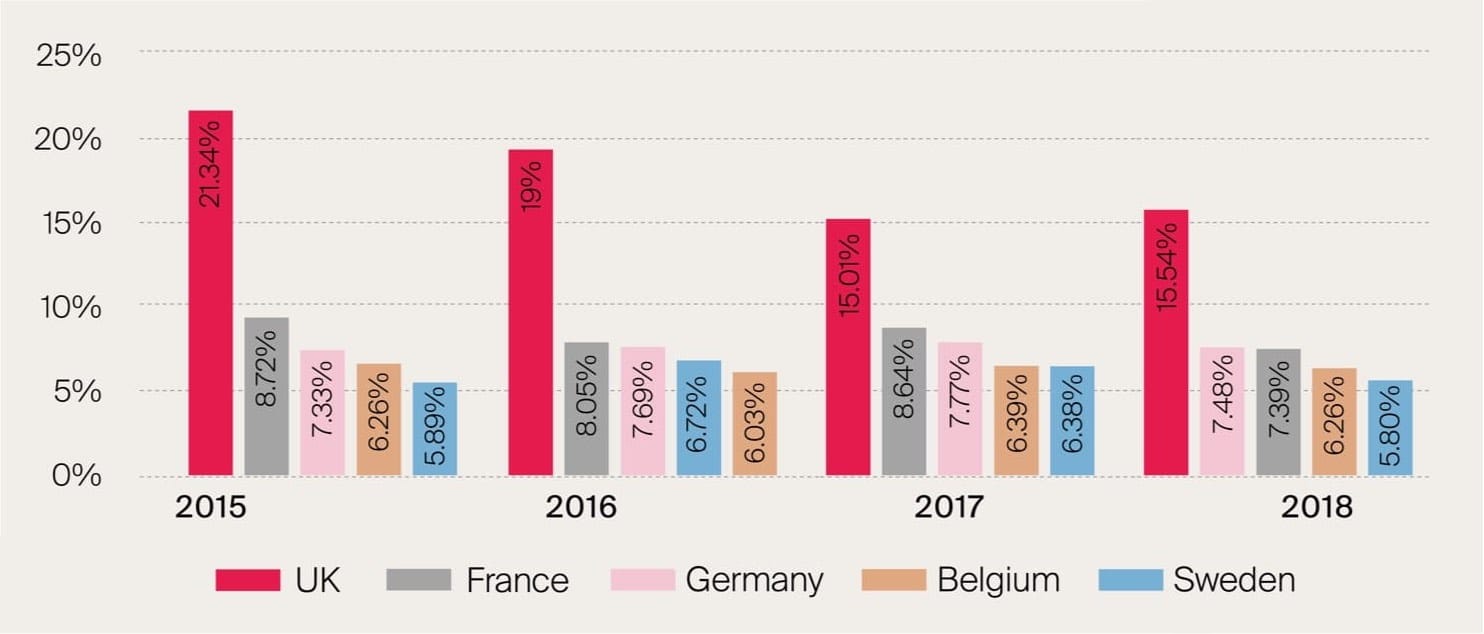

Percentage contribution of foreign buyers

Source: Colegio de Registradores de la Propiedad

External factors

In the end, an area as dependent upon the international market as this one cannot ignore the macro movements at play, be they economic, political or a combination thereof. The Catalan situation doesn’t cast a positive spell over Spain in general and Catalunya in particular, but it has driven some investment to these shores. The recent oscillations in rentals legislation and lack of tax reform have done the market no favours, but even the virtual abolition of inheritance tax within the Autonomous Region of Andalucía has had a positive knock-on effect.

Elections and referendums

We await the result of the Spanish general election, but its main impact on this region could come in the form of lowered taxes, more flexible labour laws and other business and investment-friendly measures that one would expect, not necessarily get, from a new government. Which leaves us with the elephant in the room: Brexit. The unexpected ‘decision’ (51,9%-48,1%) of the British people to separate from the European Union that followed the June 2016 referendum, saw an immediate reaction in the second half of that year as sales to British buyers dropped. The Scandinavian, Belgian, French, Middle Eastern and Eastern European markets more than compensated for this, but by 2017 British buyers were back in numbers.

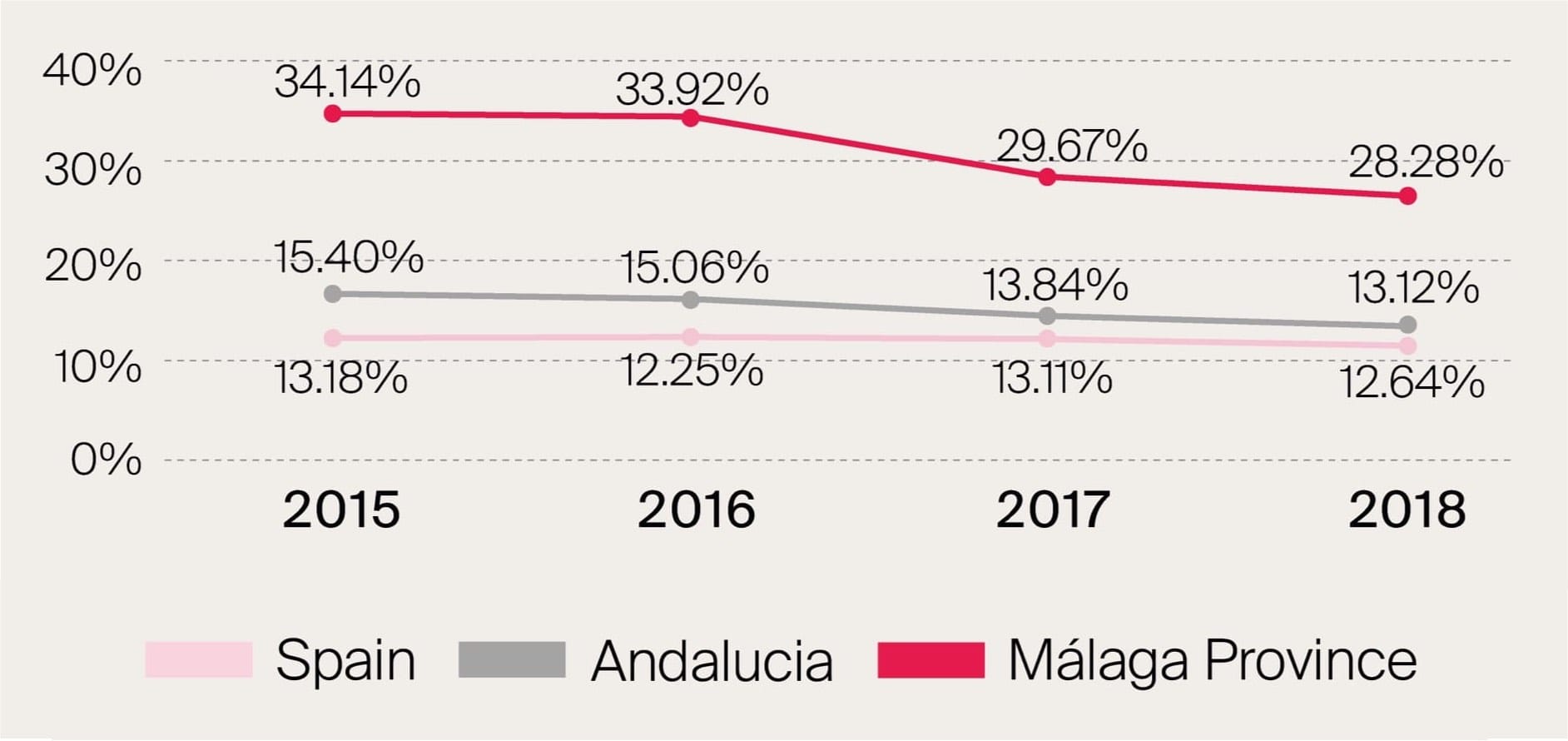

However, as Brexit began to loom as a reality the paralysis associated with its lack of clarity and direction impacted upon us once again. If in 2015 the British market still made up over 21% of foreign buyers, last year that figure fell to little over 15%. Brits are still the largest single body of non-Spanish property buyers in Marbella as elsewhere in Spain, but Brexit is reducing their market share relative to other nationalities, and will continue to do so until the divorce procedure is finally settled and known—or indeed Brexit is reversed or modified. Until then, the uncertainty will take its toll and the British market may slip from top of the table among foreign buyers who together made up 12,64% in Spain, 13,12% in Andalucía and 28,28% in Málaga province last year.

Ranking of foreign nationalities buying Spanish property (nationwide)

Percentage shows share of each nationality over the total foreign buyers for each yearSource: Colegio de Registradores de la Propiedad

Global economic winds

If the percentage of foreign buyers in Spain – which has been growing steadily for several years – slipped back under the 13% mark last year, does this indicate the rise of the domestic market or a slowing down of international demand? The answer becomes clear when you see that the actual number of property sales to foreigners rose from 61,000 in 2017 to 65,400 in 2018. This indicates that the overall market grew quite strongly. Clearly, the best markets are those with strong economic growth and high income levels, which makes the Costa del Sol relatively affordable for those from countries such as Norway, Sweden, the Netherlands and Belgium. While the pound is relatively low this won’t apply to British buyers, but in addition to price there is also the possibility of a global slowdown to ponder.

After several years of reasonably solid economic growth most economies have adjusted their output forecasts downwards a little for next year and the one to follow, pushing many below the 2% growth level that usually indicates a reasonably buoyant economy. At this point there are no cries of ‘recession’ yet, though some countries have slipped into it at least temporarily and the overall feeling is of a cooling down of economic fortunes in the near future. It’s too early to say for sure, but if we have indeed reached the end of a mild growth cycle and are headed for an equally mild slowdown this will have implications for the many new property developments reaching the market now and in the months to come.

Relative Values

How many square metres of prime property does US$1m* buy in key cities? How Though not an urban high rise market, Marbella still scores high in the sqm stakes

* All data Q4 2018 based on exchange rate on 31 Dec 2018. For Marbella, average price of prime property excludes frontline beach Sources: Knight Frank Research, Douglas Elliman, Ken Corporation, DM Properties

How the market is responding

So how does the market respond to this? If average sales times begin to grow this will eventually put pressure first on the phased price increases of off-plan projects, and ultimately result in reduced prices. We expect prices to begin to stabilise and later drop a little, as always starting with those properties that feel the pinch of competition strongest and/or are less favourably situated. So don’t expect many bargains in prime locations anytime soon.

Investors

The fact that some American and European funds, are not as active as they were a few years ago in the local market or at the very least in land banking, is an indication that the market could be slowing down, as the institutional investors who prefer steady returns to risk may be losing confidence in the short-term prospects of new projects. For one, we will have to see a cooling off of land and construction costs as well as an easing of property prices if the market is to regain its dynamism, as well as a resolution of the Brexit impasse. But that’s not to say that brave, unique and also truly luxurious initiatives can’t be successful.

Buyers

The success of projects such as Emare, Epic, Nine Lions, The Edge, The View Marbella, and similar high-spec developments in top locations offering relatively rare villa space and comfort in an apartment/penthouse configuration, shows once again that, if it’s the right fit, the top end of the market is more resilient than the broad middle belt. For this reason, many who could previously afford prime locations within Marbella/Benahavís/Estepona are now looking at less expensive ones here and in neighbouring areas. As far as our own demographics are concerned, they show that younger generations (35-44) rank first in property searches, followed by the 45-54 age bracket and 25-34 year olds are third on the list.

Developers

Creative, innovative products offered by developers who have the strength of their convictions might just fill a hitherto uncatered for niche, but that can be easily said and not done if your costs are already high and your margins tight. Need is the father of invention and creativity, so new and exciting need not always be costlier, though naturally it is riskier than the tried and tested formula that too many follow.

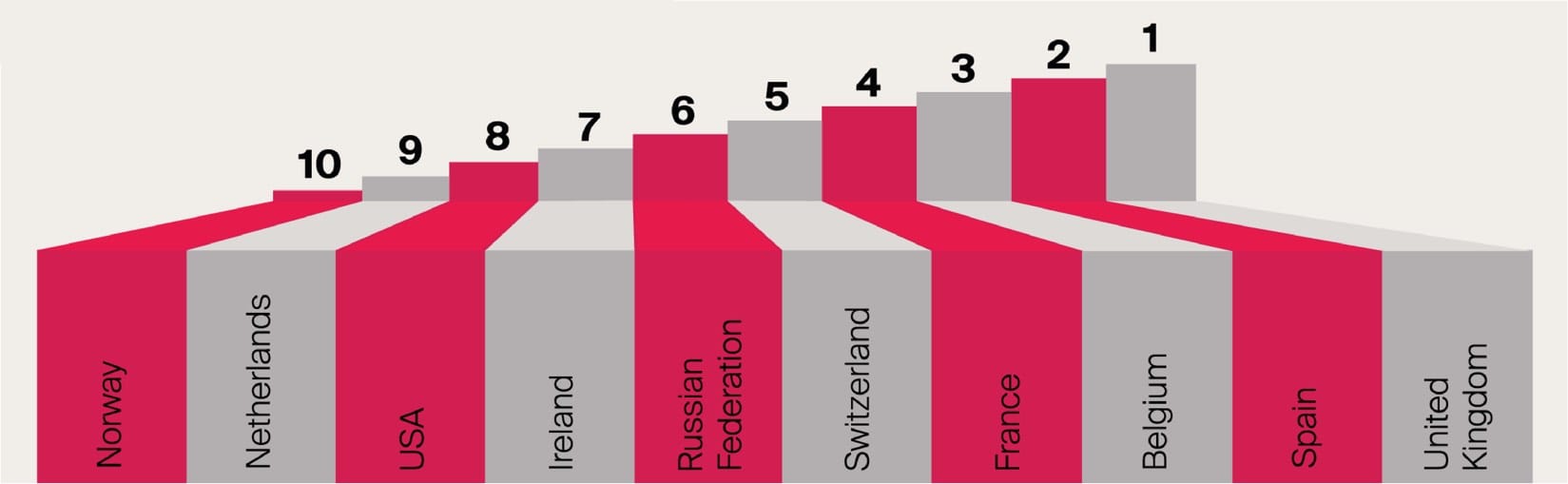

Top 10 nationalities searching for property in Marbella in 2018

Source: DM Properties|Knight Frank

The bottom line

Before we get down on ourselves, let’s be reminded that though market conditions have got a little tougher in the past few months we haven’t officially entered anything near a recession or downturn. If anything, construction, sales and rising prices will continue moderately for some time to come, but if we’re to avoid choppy waters it pays to look potential threats in the eye and be prepared for them. Not doing this in the past cost us dearly, and that is an experience most of us wouldn’t want to revisit any time soon. So let’s work at being creative, offering quality and value, and hope that price levels even out in the near future.

“We expect prices to begin to stabilise and later drop a little…”

Let’s allow the real estate offering to evolve and diversify, building on the good news of infrastructural improvements and public works, as well as solid investment into the region that will see new hotels and resorts by prestigious brands add dynamism to a tourist market that still offers homeowners 3-4% net returns on short-term holiday lets. The long-term rentals market is similarly strong and we can build on a client base for sales and rentals that is more geographically diverse than ever, so once Brexit is behind us there are more than enough reasons to remain optimistic.

")